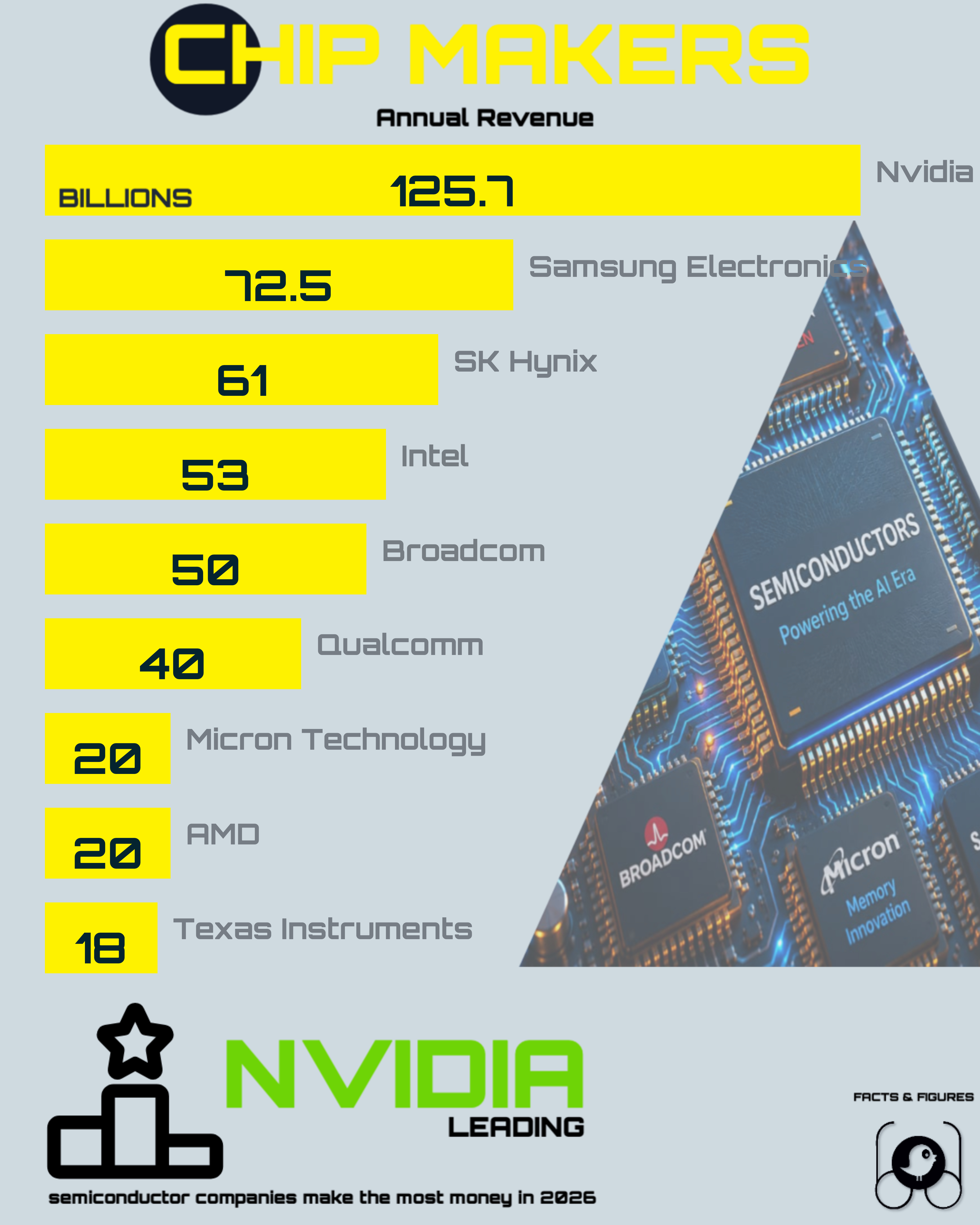

125.7B

Nvidia's $125.7B in revenue is driven by AI training and inference GPUs — the H100, H200 and Blackwell B200 — sold to hyperscalers building AI datacenters.

Facts & Figures

Visual Intelligence

Market Leader

Nvidia closed the 2025/2026 fiscal year with $125.7 billion in revenue — more than any other semiconductor company on the planet, and $53.2 billion ahead of Samsung Electronics, the closest rival by revenue on this list. Five years ago Nvidia was best known as a gaming graphics card maker; today it is the default supplier of the processors that train and run large AI models, a shift that happened almost entirely inside one product category: the datacenter GPU. The engine behind that number is a run of AI accelerator chips — the Hopper-generation H100 and H200, and the newer Blackwell B200 — that hyperscalers like Microsoft, Google, Meta and Amazon buy by the tens of thousands to build AI training clusters. Nvidia doesn't just sell silicon; it sells the CUDA software stack that most AI research and production code is written against, which makes switching to a rival GPU a much bigger decision than swapping one chip for another. That software lock-in is the real reason the revenue gap keeps widening: memory makers like Samsung and SK Hynix sell components at volume and thin margins, foundries like TSMC manufacture chips on contract for whoever pays, but Nvidia sells a full AI computing platform at premium prices, with demand currently outstripping supply. Every company in the tiers below is chasing a piece of that AI buildout — either by supplying Nvidia's chips (SK Hynix's HBM memory), competing directly with GPUs of their own (AMD), or building custom alternatives for hyperscalers (Broadcom).

Nvidia's 2025/2026 revenue is built almost entirely on AI datacenter GPUs, not the gaming cards that first made the company famous.

125.7B

Nvidia's $125.7B in revenue is driven by AI training and inference GPUs — the H100, H200 and Blackwell B200 — sold to hyperscalers building AI datacenters.

Above $50 Billion

Samsung Electronics earns $72.5 billion from a chip business built on volume rather than novelty: DRAM and NAND flash memory that ships inside nearly every laptop, smartphone and server sold worldwide. Alongside memory, Samsung runs its own foundry and designs the Exynos processors that power select Galaxy phones, making it one of the only companies that both manufactures memory at scale and competes with TSMC for foundry contracts.

Samsung's memory chips are largely invisible to consumers — nobody buys a laptop for its DRAM brand — but the company's manufacturing scale gives it real pricing power over memory cycles that affect every other device maker's costs, from PC builders to smartphone assemblers.

SK Hynix's $61.0 billion in revenue tells the story of how AI reshaped the memory business. The South Korean company is the leading producer of High Bandwidth Memory (HBM), the specialized memory stacked directly next to AI GPUs like Nvidia's H100 and H200 to feed them data fast enough to keep up with AI training workloads. Without HBM, Nvidia's chips would be bottlenecked no matter how powerful their processing cores are.

That positioning has made SK Hynix one of Nvidia's most important suppliers rather than just a competitor in the broader memory market. Standard DRAM and NAND still make up a large share of its business, but HBM's higher margins and AI-driven demand are why SK Hynix's memory revenue has climbed past longtime rival Samsung in some product categories.

Intel's $53.0 billion in revenue comes from the company that has powered the majority of the world's laptops and servers for decades through its Core and Xeon CPU lines. That dominance has narrowed as AMD and Arm-based chips gained ground, but Intel remains the default processor in most Windows PCs and a major force in datacenter CPUs, even as its share of AI-specific compute lags far behind Nvidia's.

Intel's bigger bet is Intel Foundry, its push to manufacture chips for other companies the way TSMC does, turning its own fabs into a second revenue stream. It's also selling Gaudi AI accelerators as a lower-cost alternative to Nvidia's GPUs, though neither effort has yet closed the gap with the AI chip leader.

Broadcom's $50 billion-plus in revenue comes from two very different businesses under one roof: networking chips — the switches and routers that move data inside AI datacenters — and custom AI silicon designed for specific hyperscale customers rather than sold as off-the-shelf GPUs. That custom-ASIC business has reportedly included work with Google on its in-house AI chips, positioning Broadcom as a path into AI hardware that doesn't run through Nvidia at all.

Broadcom also makes the wireless and RF chips found in iPhones and other smartphones, giving it a foothold in mobile hardware most people never see mentioned. That mix — invisible infrastructure chips plus custom AI silicon — is why Broadcom's revenue keeps climbing without a single consumer-facing product to its name.

Below $50 Billion

Qualcomm's $40 billion-plus in revenue comes almost entirely from chips that never carry the Qualcomm name to consumers. Its Snapdragon processors power the majority of Android flagship phones, and its modem chips handle cellular connectivity in devices from multiple brands — including, for years, the iPhone itself. That makes Qualcomm the closest thing the smartphone chip market has to a default supplier.

The company is now pushing into new territory with Snapdragon X Elite chips built for Windows laptops, aiming to challenge Intel and AMD on their home turf, plus automotive chips for connected and self-driving vehicle systems — a bet that mobile-style efficiency matters as much outside phones as inside them.

Micron Technology's $20 billion-plus in revenue makes it the only major memory chipmaker headquartered in the United States, competing directly with Samsung and SK Hynix in DRAM and NAND flash. Its chips ship inside PCs, smartphones, servers and increasingly AI systems, where Micron has been racing to catch up in HBM3E memory to avoid ceding the entire AI memory market to its South Korean rivals.

Memory pricing is notoriously cyclical, and Micron's revenue swings harder with those cycles than most companies on this list — a reminder that even companies supplying the AI boom aren't insulated from the boom-and-bust economics that have defined the memory business for decades.

AMD's $20 billion-plus in revenue spans three product lines: Ryzen CPUs for consumer PCs, EPYC processors that have taken meaningful server market share from Intel, and Radeon graphics cards for gamers. All of it is manufactured by TSMC rather than AMD's own fabs, since AMD sold its manufacturing arm — now GlobalFoundries — back in 2009 to focus purely on chip design.

AMD's MI300 series is its answer to Nvidia in AI accelerators, and it's the closest thing to a credible alternative on the market — but Nvidia's CUDA software ecosystem still gives it a head start AMD hasn't fully closed, which is the main reason AMD's AI chip revenue remains a fraction of Nvidia's.

Texas Instruments reports $15 to 18 billion in revenue from chips most people have never heard of and will never buy directly: analog and embedded processors that manage power, sense temperature and pressure, and control basic electronics inside cars, industrial equipment and appliances. It's the least AI-driven business on this list, and one of the most stable — TI's chips don't chase hype cycles.

That steadiness is the point: TI's products go into things that need to work reliably for a decade or more, from factory sensors to automotive safety systems, making it less exciting to hardware enthusiasts but arguably more essential to the physical world running smoothly.

Data Table

Every chipmaker from Nvidia's $125.7B down to Texas Instruments' $15-18B, in one list — company, reported 2025/2026 revenue, and the chip category each one is best known for.

| 1 | Nvidia | $125.7 billion | AI processors, Datacenter GPUs |

| 2 | Samsung Electronics | $72.5 billion | Memory Chips (DRAM, NAND), Consumer Electronics |

| 3 | SK Hynix | $61.0 billion | AI memory, HBM (High Bandwidth Memory) |

| 4 | Intel | $53.0 billion | CPUs, Foundry services, AI accelerators |

| 5 | Broadcom | $50+ billion | Networking components, Custom ASICs |

| 6 | Qualcomm | $40+ billion | Mobile processors, Wireless RF |

| 7 | Micron Technology | $20+ billion | DRAM and NAND Flash memory |

| 8 | AMD | $20+ billion | CPUs, Datacenter GPUs |

| 9 | Texas Instruments | $15–18 billion | Analog and embedded processing |

Figures shown as "$50+ billion" or as a range (Texas Instruments' $15-18B) are approximate thresholds from original company disclosures, not exact totals — treat them as directional rather than precise when comparing close scores like Broadcom and Qualcomm.

AI Chip Leadership

Nvidia's H100 and Blackwell B200 GPUs are the default hardware inside almost every major AI training cluster, from OpenAI's infrastructure to Microsoft, Google and Meta's in-house datacenters. That dominance isn't just about raw chip performance — it's the CUDA software platform built up over nearly two decades that makes Nvidia hardware the easiest, best-supported choice for AI research and production workloads, which is why rivals with genuinely competitive chips still struggle to take meaningful share.

Buyer's Guide

For most people buying hardware specifically for AI work — training models, running local LLMs, or heavy machine-learning workloads — Nvidia is still the safe default, purely because of CUDA's software support; almost every AI framework and tutorial assumes an Nvidia GPU first. AMD's Radeon and MI300 chips are a legitimate, cheaper alternative if you're comfortable working around occasional software gaps, and Apple Silicon's unified memory makes it a strong pick for running smaller models locally on a laptop. Intel and Qualcomm remain better bets for general-purpose computing than for AI-specific acceleration, at least for now.

The revenue figures in this ranking were collected and compiled manually from the official investor relations pages and annual reports of each listed company — Nvidia, Samsung Electronics, SK Hynix, Intel, Broadcom, Qualcomm, Micron Technology, AMD and Texas Instruments. Full credit for the underlying financial disclosures belongs to each company's own investor relations team.

FactsFigs reviews, cleans, and cross-checks every source dataset before shaping it into a data story. Each visualization is created and designed in FactsFigs Design Studio — an internal tool developed and owned by FactsFigs — and is the original work of a FactsFigs author, not an AI-generated copy of any existing graphic. Individual assets within a visual may or may not be produced with AI tools, but the design of the visual itself is solely FactsFigs' own.

Figures are estimates at the time of publication, provided for information only — nothing here is financial advice or a guarantee of accuracy.

Last verified: 17 July 2026

Related Publications

Storage got a million times cheaper from 1980 to 2022 — then a 2025 NAND shortage sent SSD prices climbing again while HDDs kept falling.

06 Aug 2026

The base iPhone price moved only twice between 2017 and 2025 — once downward. What climbed was the ceiling: new premium tiers, not blanket increases.

04 Aug 2026

The $20 entry price for AI subscriptions held from 2023 to 2026 while the ceiling climbed to $200 — and $300 at Grok.

10 Aug 2026

Nintendo, PlayStation and Xbox launch prices in 2026 dollars: sticker prices rose, but real prices fell 22% to 36% since launch.

07 Aug 2026